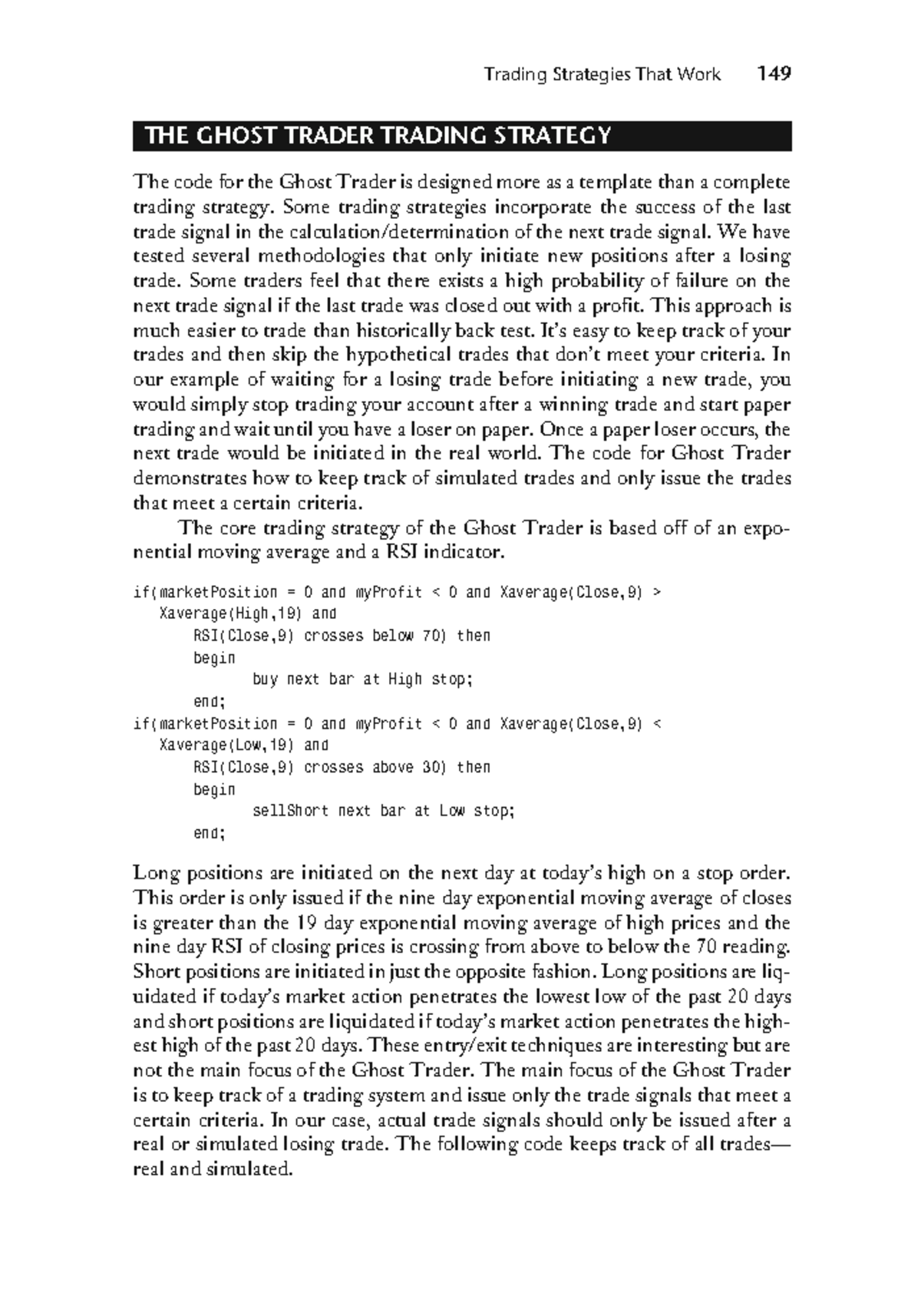

Equity markets have a short memory and a desperate need for oxygen. On Friday, the pan-European STOXX 600 index clawed back 1.5%, while Germany’s DAX and France’s CAC 40 both leaped roughly 2% in a display of collective relief. The catalyst was a single, calculated post on X from Iranian Foreign Minister Abbas Araghchi, declaring the Strait of Hormuz "completely open" for commercial shipping.

Travel and leisure stocks led the charge, with some sectors gaining 5% in a single session. To the casual observer, the crisis that had strangled global energy markets since March 4, 2026, appeared to be over. But for those watching the fundamentals, this rally looks less like a recovery and more like a tactical pause in a much larger economic siege.

The Illusion of Normalcy

The markets are currently pricing in a "best-case scenario" that ignores the physical reality of energy logistics. While Tehran has eased the maritime blockade, the damage to the global supply chain is not something that vanishes with a press release. Brent crude, which had rocketed past $120 per barrel during the height of the closure, plunged 10% on the news. This drop is the primary fuel for the stock surge, particularly for airlines like Lufthansa and Air France-KLM, which saw their valuations decimated over the last six weeks.

The sudden reopening is a relief valve, but it is not a repair. During the closure, QatarEnergy was forced to declare force majeure on liquefied natural gas (LNG) exports. Those cargoes do not just reappear overnight. The maritime traffic jam backed up in the Gulf of Oman and the Persian Gulf will take weeks to clear, and insurance premiums for hulls traversing the 21-mile-wide choke point remain at prohibitive levels.

Investors are buying the headline, but they are ignoring the ledger. The European Central Bank (ECB) already slashed growth projections for 2026 and raised inflation forecasts in response to the initial shock. One afternoon of green candles on a trading screen does not undo the fact that European gas storage levels hit a historic low of 30% this spring.

Why Travel Stocks Are a Dangerous Bet

The 5% jump in travel stocks is built on the assumption that the summer season is saved. This is a fragile premise. The International Energy Agency (IEA) recently warned that Europe’s jet fuel reserves were down to a six-week supply. While crude oil is moving again, the refining process for kerosene-based products cannot be instantly accelerated to meet the demands of the peak holiday window.

Airlines are facing a pincer movement. On one side, they have the high cost of fuel already purchased during the spike. On the other, they face a consumer base whose discretionary income is being eaten alive by 30% surcharges on electricity and industrial goods.

The Refined Product Deficit

The war more than doubled the price of diesel and jet fuel. Even as crude prices retreat, the "crack spread"—the difference between the price of crude oil and the products refined from it—remains historically wide. Refineries in Europe were already operating at near-capacity before the conflict; they lack the flexibility to absorb the sudden return of supply without technical bottlenecks.

- Lufthansa and IAG: Benefited from the Friday surge but remain vulnerable to labor strikes as inflation devalues employee wages.

- Airbus and Safran: Gained between 4% and 6% on hopes of normalized industrial output, yet they still face a broken mid-tier supply chain where smaller component manufacturers are teetering on insolvency due to energy costs.

The Geopolitical Toll Booth

The most overlooked factor in this "reopening" is the new precedent set by Tehran. During the conflict, Iran floated the idea of transit fees for vessels crossing the Strait. Even if these are not formalized tomorrow, the threat of a permanent maritime "toll booth" hangs over the market.

If shipping companies have to bake a "geopolitical tax" into every voyage through Hormuz, the long-term cost of transport for 20% of the world’s oil and LNG will be permanently higher. This isn't a temporary spike; it’s a structural shift in the cost of doing business. The markets are celebrating the end of a blockade, but they are failing to see the birth of a more expensive, less predictable era of maritime trade.

The ECB Dilemma

The stock market’s exuberance also creates a headache for the European Central Bank. The ECB had been signaling a move toward lower interest rates before the March 4 blockade. The energy shock forced them to pivot back to a hawkish stance to combat the resulting inflation.

Now, with stocks surging and the immediate threat to the Strait receding, the "stagflation" narrative has softened. However, if the ECB interprets this market rally as a sign of economic resilience, they are less likely to provide the interest rate cuts that the broader economy—particularly the struggling construction and retail sectors—desperately needs.

The rally in bank stocks, with Santander and BNP Paribas gaining over 4%, is a bet on this exact tension. Banks win when rates stay high, but the industrial giants they lend to eventually break under the pressure.

Beyond the Headline

The reality of April 2026 is that Europe has just survived a heart attack, and the patient is currently experiencing a "dead cat bounce" in confidence. The structural vulnerabilities revealed by the 2026 Iran war—the over-reliance on a single maritime artery and the lack of energy sovereignty—remain entirely unaddressed.

The Strait is open, for now. But the geopolitical leverage has shifted. Iran has demonstrated it can crash the global economy at will and then "save" it with a tweet, reaping the diplomatic rewards of de-escalation without giving up any of its strategic advantages.

Investors who are diving back into the STOXX 600 at these levels are betting that the ceasefire is permanent and that the energy crisis was a one-off event. History, and the current state of European fuel reserves, suggests otherwise. The smart money isn't chasing the 5% gain in travel stocks; it’s looking for the exit before the next bottleneck forms.

Watch the jet fuel storage levels in Rotterdam and the "force majeure" status of Qatari shipments. Those are the real indicators. The rest is just noise on a Friday afternoon.